Skip Maine state header navigation

INDIVIDUAL INCOME TAX

Schedule NR

Worksheet A

Worksheet B

for

Part-year Residents/Nonresidents/Safe Harbor Residents

GUIDANCE

DOCUMENT

Maine

Revenue Services, Income/Estate Tax Division

Last Revised: December 2019

SCHEDULE NR

PART-YEAR RESIDENTS, NONRESIDENTS and

“SAFE HARBOR RESIDENTS” ONLY

If you are a part-year resident of Maine and

received income during that part of the year you were a resident of Maine, or,

during any period of nonresidency, had income from Maine sources resulting in a

Maine income tax liability, you must file Maine Form 1040ME.

Exceptions

·

Minimum taxability thresholds. A nonresident individual working in Maine as an employee

is not required to pay a Maine tax or file a Maine return on income from

personal services unless that individual works in Maine for more than 12 days and

earns or derives income from all Maine sources totaling more than $3,000. Up to 24 days performing certain personal

services, such as training and site inspections, are not counted against the

12-day threshold. Also, generally, a

nonresident individual present in Maine for business for no more than 12 days

and earning no more than $3,000 from business activity in Maine is not required

to pay a Maine tax or file a Maine return on that income.

·

Political subdivision employee.

Income earned by a nonresident employee

of a political subdivision of an adjoining state performing services in Maine

in accordance with an interlocal agreement under 30-A M.R.S., Chapter 115 is

not considered Maine source income, so long as the work performed does not

displace a Maine resident employee.

·

Declared state disaster or

emergency. Compensation or income directly

related to a declared state disaster or emergency is exempt from Maine tax if

the taxpayer’s only presence in Maine during the tax year is for the sole

purpose of providing disaster relief.

See 36 M.R.S. §§ 5142(8-B) and 5142(9) and Rule 806.

For information regarding

residency status, refer to the “Guidance to Residency Status” brochure

and the “Guidance to Residency Safe Harbors” brochure at www.maine.gov/revenue/incomeestate/guidance.

Part-year residents, nonresidents and “safe harbor”

residents who receive income from outside Maine during the period of nonresidence may be able to claim a nonresident

credit. This credit is calculated on

Schedule NR using Worksheet A, Worksheet B and, if necessary, Worksheet C. Full-year residents of Maine may not claim a

nonresident credit and should not complete Schedule NR. Do not file Schedule NR if all your

income is taxable by Maine.

Part-year residents, nonresidents and “safe harbor”

residents must include a complete copy of their federal return (including all

schedules and worksheets) with the Maine return, even if they are not eligible

to claim a nonresident credit.

Part-year residents, nonresidents and “safe harbor” residents must file

a Maine income tax return using the same filing status as properly used on the

federal income tax return and must complete Form 1040ME and Schedule NR. However, do not use Schedule NR if all

your income is taxable to Maine. If one

spouse is a full-year Maine resident and the other spouse is not, and a joint

federal return was filed, you have two options:

1) You can choose to file a joint Maine income

tax return as if both were full-year Maine residents, in which case, you may

qualify for the Credit for Income Tax Paid to Other Jurisdictions; or

2) Each spouse may file a Maine income tax return

as a single individual using Form 1040ME with Schedule NRH. For more information, see Form 1040ME,

Schedule NRH and the Instructional

Pamphlet for Schedule NRH at www.maine.gov/revenue/incomeestate/guidance.

Each income tax return must show the proper residency status. You may choose this option only if you

filed a joint federal return.

If the nonresident, or “safe harbor” resident spouse has

no Maine source income, that spouse does not have to file a Maine Return.

If one spouse is a full-year Maine resident and the other

spouse is a nonresident, the Maine resident spouse must file as a single

individual using Schedule NRH. See the Instructional Pamphlet for Schedule NRH

at www.maine.gov/revenue/forms for examples

of when to file Schedule NRH.

If both spouses are nonresidents or

“safe harbor” residents, and a joint federal income tax return was filed, but

only one spouse has Maine source income, you have two options:

1) You can choose to file a joint Maine income

tax return and determine your joint tax liability as nonresidents using Form

1040ME with Schedule NR; OR

2) The spouse who has Maine source income can

choose to file as a single individual using Form 1040ME with Schedule NRH.

For more information, see Form 1040ME,

Schedule NRH.

Maine taxable income is equal to federal adjusted gross

income adjusted by Maine income modifications, exemptions and deductions. Your tax is first calculated as if you were a resident of

Maine for the entire year. Part-year

residents, nonresidents and “safe harbor” residents must then claim a

nonresident credit calculated on Schedule NR using Worksheets A and B,

and if necessary, Worksheet C based on the income that was earned

outside Maine while a nonresident of Maine.

NOTE: Nonresident or “safe

harbor” resident service members, see below for special instructions.

·

Do

not begin the Maine return with only the income earned in Maine. You must begin your Maine income tax return

with the total federal adjusted gross income.

·

Unless

specifically instructed, do not subtract the income earned outside Maine as a

negative income modification on Form 1040ME, Schedule 1.

Schedule NR is designed to separate a part-year

resident’s, nonresident’s or “safe harbor” resident’s income between Maine

source income and non-Maine source income.

Maine source income includes the following:

1) All income received while a resident of

Maine;

2) Salaries and wages earned working in Maine,

including any taxable benefits related to those earnings, such as annual and

sick leave, unless otherwise excepted. See Exceptions above. Also see 36 M.R.S. §§ 5142(8-B) and 5142(9)

and Rule 806;

3) Income derived from or connected with the

carrying on of a trade or business within Maine (including distributive share

of income (loss) from partnerships and S corporations operating in Maine),

unless otherwise excepted. See

Exceptions above. See 36 M.R.S. §§

5142(8-B) and 5142(9) and Rule 806;

4) Shares of trust and estate income derived

from Maine sources;

5) Income (loss) attributed to the ownership or

disposition of real or tangible personal property in Maine. NOTE:

For tax years beginning on or after January 1, 2019, nonresident

individual taxpayers may elect to recognize the entire gain from an installment

sale of real or tangible property located in Maine in the taxable year of the

transfer or the remaining gain in a subsequent taxable year to the extent the

gain has not been reported in a previous tax year. Once made, the election is

irrevocable;

6) Maine source gain (or loss) from the sale of

a partnership interest. NOTE: To determine the gain or loss from the sale of

a partnership interest attributable to Maine, divide the original cost of all

tangible property of the partnership located in Maine by tangible property

everywhere. Tangible property includes

real estate, inventory and equipment. If

you don’t know these amounts, contact the partnership. If more than 50% of the partnership’s assets

consist of intangibles, the gain (or loss) is allocated to Maine based on the

sales factor of the partnership. Divide

the sales in Maine for the last full tax year of the partnership preceding the

year of sale by the total sales for that same year. Multiply the result by the gain or loss on the

sale of the partnership interest reported on your federal return. “Sales” for purposes of computing the sales

factor are defined in Rule 801. Include

the gain (or loss) from the sales of a partnership interest on Worksheet B,

Column E, line 6; and

7) Maine State Lottery or Tri-State Lottery

winnings from tickets purchased within Maine, including payments received from

third parties for the transfer of rights to future proceeds related to Maine

State Lottery or Tri-state Lotto tickets purchased in Maine, plus all other

income from gambling activity conducted in Maine.

Except for Item #6 above, income from intangible sources,

such as interest, dividends, annuities, most pensions and gains or losses

attributable to intangible personal property, received by a nonresident of

Maine is not Maine source income unless it is attributable to a

business, trade, profession or occupation carried on in Maine.

Instructions for

completing 2019 Form 1040ME, Schedule NR

A part-year resident is subject to Maine income tax on

all income derived while a resident of Maine, even if the income is received

from out-of-state sources, plus any income derived from Maine sources during

the period of nonresidence.

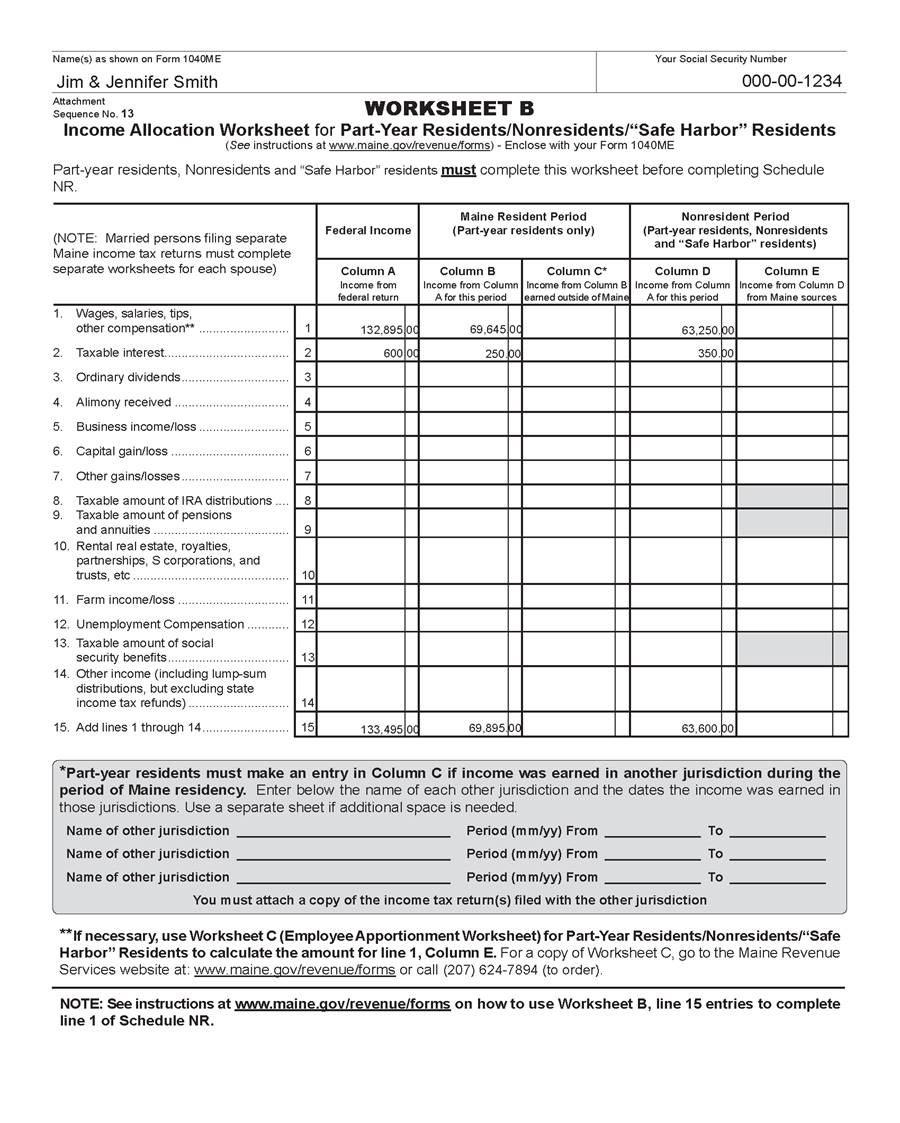

Form 1040ME, Worksheets A and B, available at www.maine.gov/revenue/forms, must be completed prior to

completing Schedule NR. Follow the

step-by-step instructions for completing Schedule NR available at www.maine.gov/revenue/forms.

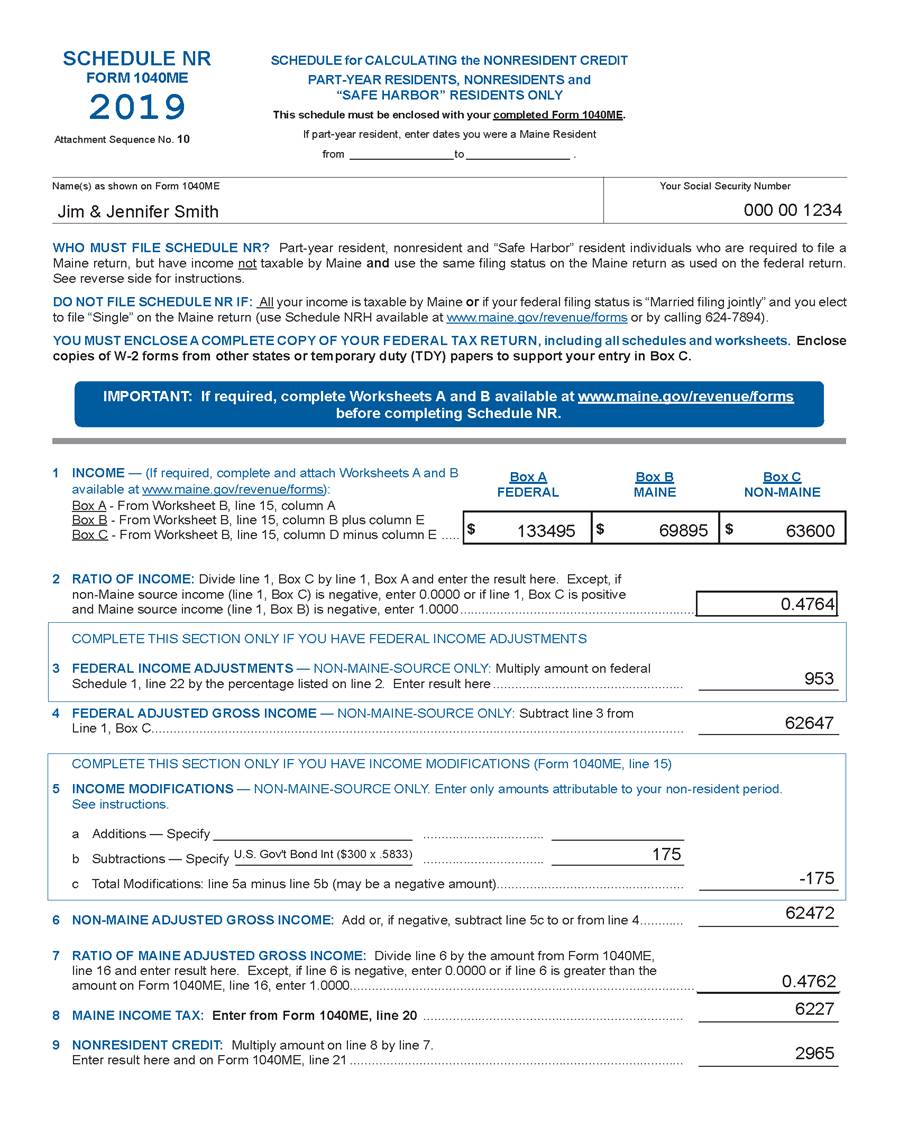

Form 1040ME, Schedule NR, line 1. (Nonresident and “Safe Harbor” resident

service members, see below for special instructions.) After you complete Form 1040ME through line 20a

based on your total federal adjusted gross income, complete Schedule NR to

calculate the amount of your nonresident credit. To complete Schedule NR, line 1:

1) Enter your total federal income in Box A (from

Worksheet B, column A, line 15).

2) Enter all Maine source income in Box B,

including any income earned in Maine while a nonresident or “safe harbor”

resident of Maine (Worksheet B, column B, line 15 plus Worksheet B, column

E, line 15).

3) Enter all non-Maine source income in Box C (Worksheet

B, column D, line 15 minus Worksheet B, column E, line 15). If you included a taxable state income tax

refund on your federal income tax return, do not include that

refund when completing Worksheet B or Schedule NR.

Form 1040ME, Schedule NR, line 2.

If the ratio of non-Maine income to total income calculated on Schedule

NR, line 2, is less than 0%, enter 0.0000.

If the ratio is 100% or greater, enter the ratio like this: 1.0000. You may not claim a negative nonresident

credit or a nonresident credit that is more than your tax liability otherwise

due to Maine. You should always extend

the percentage calculations four digits beyond the decimal point; for example,

5.00% (.0500), 25.25% (.2525) or 100.00% (1.0000).

Form 1040ME, Schedule NR, line 3.

To complete Schedule NR, line 3, Federal Income Adjustments, multiply

the amount of federal income adjustments from

non-Maine sources listed on federal Form 1040 or Form 1040-SR, Schedule 1, line

22, by the percentage calculated on Schedule NR, line 2.

Form 1040ME, Schedule NR, line 5.

(Nonresident and “Safe Harbor” resident service members, see below for

special instructions.) If you have

completed Form 1040ME, Schedule 1, Income Modifications, you must

complete Schedule NR, line 5. Enter the

amount of income modifications from non-Maine sources on Schedule NR,

lines 5a and 5b as they apply.

Generally, for a part-year resident, the amount of the non-Maine source

income modification that is from intangible sources (interest, dividends,

annuities, etc.) is calculated by multiplying the income by the percentage of

the year you were a nonresident. For

example, if you were a nonresident for 9 months of the year, you would enter on

Schedule NR, lines 5a and 5b as applicable, 75% (9 months divided by 12 months)

of the income modifications reported on Maine Schedule 1.

· Do not include taxable refunds of

state and local taxes.

· Prorate the pension deduction (Form

1040ME, Schedule 1, line 2d) based on the percentage of qualified pension

income received as a nonresident.

Form 1040ME, Schedule NR, line 9.

After completing Schedule NR, any nonresident credit on line 9 is

entered on Form 1040ME, line 21. This

credit will reduce your Maine taxes for income not taxable to Maine.

· If you are a nonresident of Maine, and

your only income from Maine sources are losses, you do not need to file an

income tax return with Maine, because you have no Maine income tax

liability. However, you may choose to

file a return with Maine if you expect to have positive income from Maine

sources in future years and want to avoid having gaps in your filing history.

· You may not use Maine losses in a

prior year to offset Maine income in the current year unless those losses also

appear on the federal return for the current year or the loss relates to NOLs

disallowed in 2009 - 2011 or to a federal NOL carryback disallowed for Maine

income tax purposes. (Federal NOL

carrybacks with respect to NOLs realized in tax years beginning after 2001 are

not allowed for Maine purposes. The

disallowed NOL carryback may be recovered in the allowable carryover period.)

· For additional information on

determining what types of income are subject to Maine tax when received by a

nonresident, see Rule 806 available at www.maine.gov/revenue/rules/.

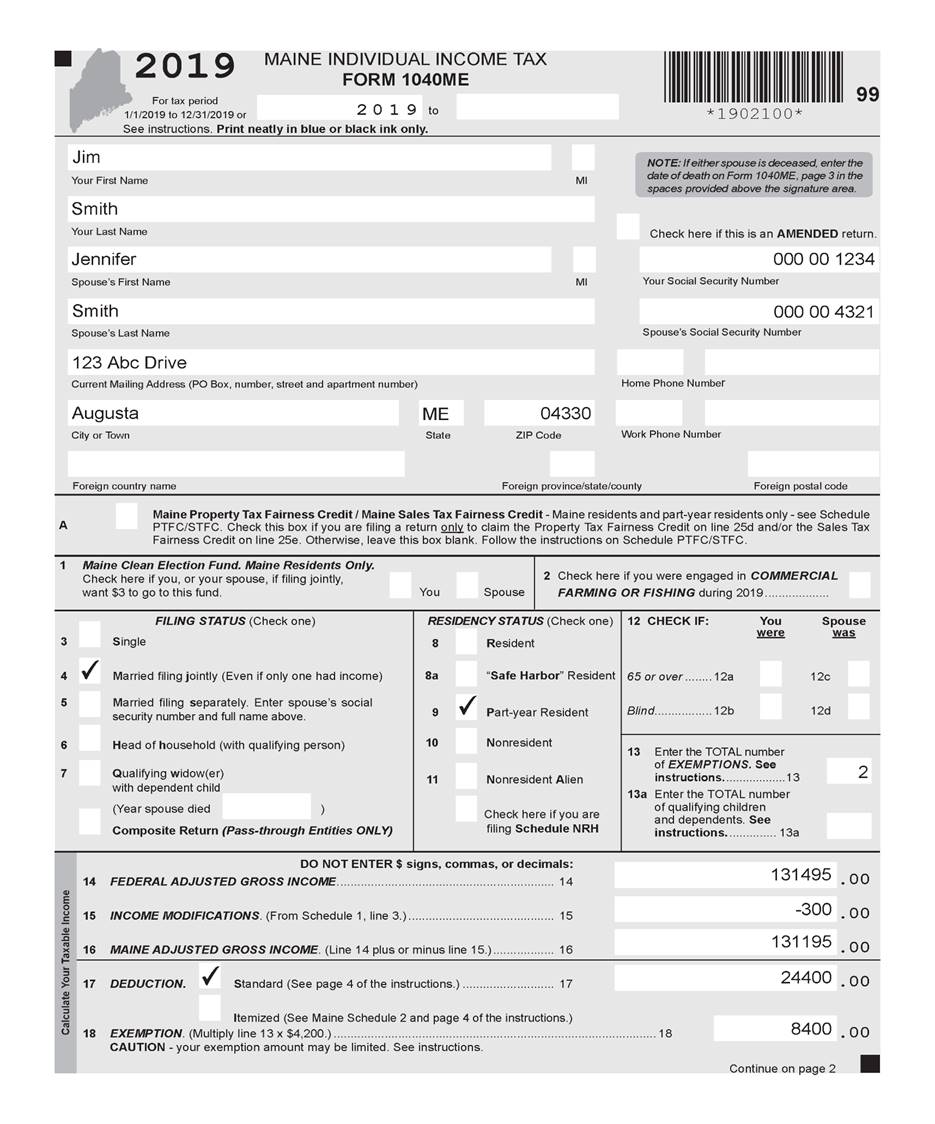

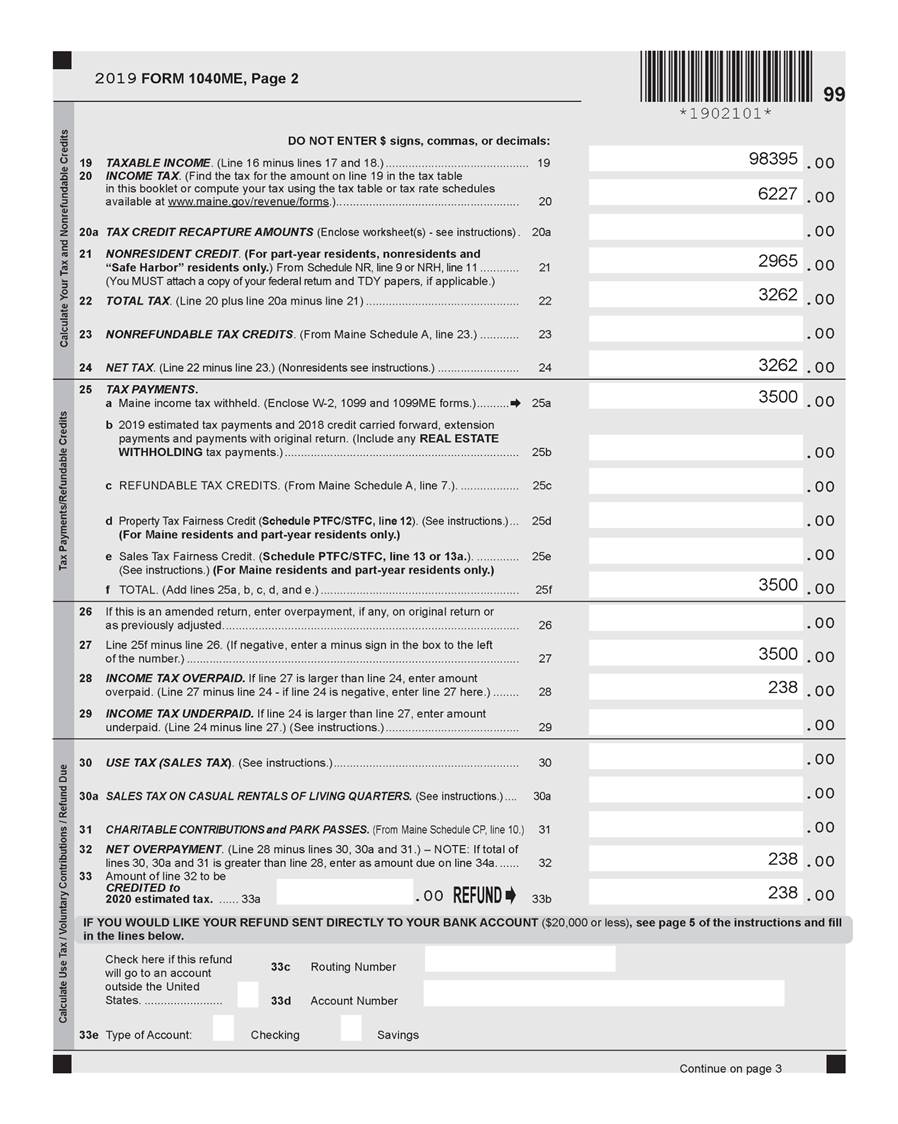

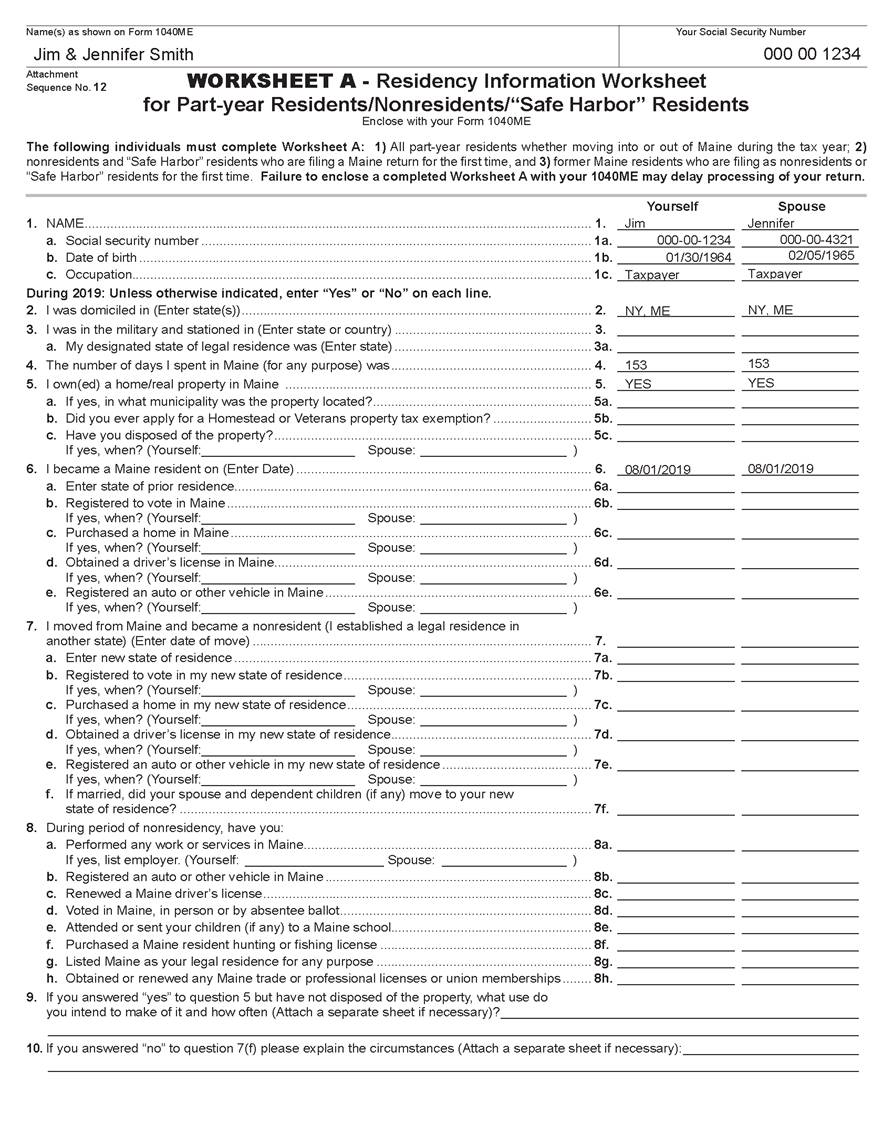

Attached is a

sample return for a part-year resident.

The instructions in the Form 1040ME booklet and this pamphlet are used

to complete a Maine return for the Smiths based on the information below:

Jim and Jennifer Smith are from New York. Jim works as an analyst for a large

bank. Effective August 1, 2019, Jim was

transferred to Maine while working for the same employer. Jim and his family moved to Maine and became

residents of Maine on August 1, 2019.

After coming to Maine, Jennifer got a job as a supervisor in a local

production facility.

In 2019, Jim earned a total of $107,895 in

wages from the bank. He earned $63,250

in New York and $44,645 in Maine.

Jennifer earned $25,000 from her job in Maine. From Jim’s pay, $3,200 was withheld for New

York income taxes and $2,250 was withheld for Maine income tax. Jennifer had $1,250 withheld from her pay for

Maine. The Smiths had $600 in interest income

throughout the year, $300 of which came from U.S. Government bonds.

The Smiths filed a married joint federal

income tax return for 2019 and reported federal adjusted gross income of $131,495.

NONRESIDENT

& “SAFE HARBOR” RESIDENT SERVICE MEMBERS

The Servicemembers Civil Relief Act

“SCRA” (Public Law No. 108-189) provisions offset the computation of Maine

individual income tax for certain nonresidents (including “Safe Harbor”

residents) as follows:

1) Section 511(d) of the Act prevents states

from including the military compensation of nonresident service members in the

total income when computing the applicable rate of tax imposed on other income

earned by the nonresident service member, or their spouse, that is subject to

tax by the state. This change affects Maine

returns filed for tax years beginning on or after January 1, 2003 for some

military taxpayers (Maine returns filed for tax years beginning on or after

January 1, 2007 for “Safe Harbor” residents).

2) Amendments were made to the SCRA in 2009 for

tax years beginning on or after January 1, 2009 to provide that a spouse of a

service member may retain residency in their home state for tax purposes if the

spouse is in Maine solely to be with the service member who is in the state due

to military orders. The SCRA was further

amended in 2018 for tax years beginning on or after January 1, 2018 to provide

that a spouse of a service member may adopt the home of record of their

military spouse for tax purposes. Income

earned in Maine by a nonresident service member’s spouse who is domiciled in

another state may not be considered Maine source income.

Since the 2019 Maine income tax return includes income of the

nonresident service member, a deduction must be made on the Maine return for a

nonresident (or “Safe Harbor” resident) service member. To deduct the military income of a

nonresident (or “Safe Harbor” resident) service member from the Maine taxable

income in 2019, use the following instructions:

1) Enter the total federal adjusted gross income

on Form 1040ME, line 14.

2) Complete Form 1040ME, Schedule 1 (see line 2e).

3) Complete Form 1040ME, lines 15 through 20a.

4) Complete Form 1040ME, Worksheet A (if applicable) and Worksheet B for Part-Year Residents/Nonresidents / “Safe Harbor” Residents. NOTE: When completing Worksheet B, include the military compensation received by the nonresident (“Safe Harbor” resident) service member and the Maine earned income of the service member’s spouse on line 1, columns A and D. This procedure will ensure the proper determination of non-Maine source income.

5) Complete Form 1040ME, Schedule NR.

NOTE: The military income of a nonresident (“Safe Harbor”

resident) service member should be included on both line 1, boxes A and C and

line 5b of Schedule NR. On

line 5b, write “NR military compensation” in the space provided.

The Maine earned income of

the service member’s spouse should be included on line 1, boxes A and C of

Schedule NR.

This procedure will ensure

the proper ratio for the determination of the non-resident credit.

If you are completing

Schedule NRH, see the Guidance Document titled “Instructional Pamphlet for Individual

Income Tax, Schedule NRH” for more information.

6) Complete Form 1040ME, lines 21 through 34.

A “service member” is defined as a

member of the United States Army, Navy, Air Force, Marine Corps, Coast Guard, a

commissioned officer of the Public Health Service or the National Oceanic and

Atmospheric Administration. It also

includes a member of the National Guard who is under a call to active service

authorized by the President or the Secretary of Defense for a period of more

than 30 consecutive days for purposes of responding to a national emergency

declared by the President and supported by Federal funds.

Any further questions about the

computation of Maine individual income tax for certain nonresidents should be

directed to the Income/Estate Tax Division of Maine Revenue Services at: income.tax@maine.gov

or call 207-626-8475.